By Rosemary Pearson March 20, 2025

Starting a business can be challenging, especially when choosing between sole proprietorship, partnership, or corporation. Limited liability companies (LLCs) offer an alternative structure, offering limited liability protection for owners.

Illegal activities or company bankruptcy, however, can violate this. LLCs combine the features of corporations and sole proprietorships or partnerships, with liability protection but with profits and losses flowing through to owners. They are flexible with governance and tax elections decided in the operating agreement.

Understanding Limited Liability Company

Starting an LLC is simpler than starting a corporation and gives more flexibility and protection to its owners. LLCs can choose not to pay federal taxes directly, instead reporting profits and losses on the owners’ personal tax returns. They can also decide to be taxed like a corporation. If there is fraud or if legal rules are not followed, creditors might be able to pursue the members.

An LLC is different from an ULC ( Unlimited Liability Corporation ), which is allowed in some countries and Canadian provinces. An LLC has features of both a corporation and a partnership or sole proprietorship, depending on the number of owners. It shares limited liability with corporations and has pass-through taxation like partnerships. LLCs are often more flexible than corporations and work well for single-owner businesses.

In the U.S., courts generally treat LLC members similarly to corporate shareholders regarding legal protections, but it is harder to challenge the protection of an LLC because they have fewer formal requirements. Membership interests in LLCs are well-protected through special legal rules.

Advantages and Limitations of LLC

Advantages

- An LLC is a type of organization in the United States that protects its members from being liable for the company’s debts. Members usually lose only what they invested in the LLC if the business fails. If the LLC chooses partnership tax treatment, its profits, and losses are declared on the members’ individual tax returns using Schedule K-1.

- One advantage of an LLC is its simplicity. Single-member LLCs can pay taxes like sole proprietorships, so earnings are taxed only once on the owner’s personal return. LLCs have fewer operating rules than corporations, allowing members to make collective decisions with ease.

- An LLC also shields personal assets in the event of legal issues. Unlike corporations, LLCs have less restrictive ownership and management rules, permitting numerous members and flexible governance. LLCs afford more control to those running the business and are less beholden to shareholders and boards of directors.

- Furthermore, LLCs let members determine how to share profits based on their contributions or past work, making them an appropriate structure for enterprises in America.

- LLCs can choose how they can be taxed, which gives them flexibility. A multi-member LLC can share profits and losses in ways other than just based on ownership percentage, unlike S corporations that cannot do this. The members of an LLC are shielded from some or all liabilities for the LLC’s actions and debts, depending upon the state regulations.

- A S corporation is limited to 100 shareholders, and they must all be U.S. residents and tax residents. An LLC can have unlimited members without citizenship restrictions. LLCs also require much less documentation than corporations.

- LLCs usually have taxation which is pass-through, meaning profits have to be taxed during the member level, and not during the LLC level. LLCs are treated as disassociates from their members in most states. However, in some places, like Connecticut, for the LLC’s actions, members are personally liable

- LLCs can be formed with only one person. They also protect against being taken over by aggressive investors. For certain businesses, like real estate, each property can be held by a distinct LLC, safeguarding the owners and their other assets from legal concerns.

- LLCs can have different kinds of owners. These can be people, groups of people, trusts, or even other businesses. Most states don’t limit the kind or number of owners an LLC can have.

Disadvantages

- While limited liability companies offer protection from certain legal issues, their advantages are not absolute. Owners who neglect proper procedures may still face liability in court. LLCs also present tax complexities, like varying rules between states, higher formation costs, restricted ownership transfers, and additional levies on shared earnings.

- Most jurisdictions do not mandate operating agreements for LLCs, yet groups with multiple members risk disputes without establishing internal governance. As states seldom provide comprehensive default regulations, members must craft their own accords.

- Securing funding as an LLC can prove difficult since venture capitalists prefer investable entities. One workaround involves incorporating and then absorbing the LLC. Some states assess franchise or profit taxes, or levy fees dependent on owner count. Texas overhauled its system in 2007, but most retain nominal annual charges.

- Certain states, such as Maryland, burden LLCs with steep renewal fees, with charters costing $120 initially and renewals at $100. Likewise, New York mandates notices of formation that can inflate expenses in urban centers.

- LLCs face flexibility in leadership structures, needing no board. International treatment of U.S. LLCs also varies, sometimes resembling corporations for tax handling. Varied internal titles may confuse outsiders as to contractual signatory roles.

LLCs and Their Types

The owners of a Limited Liability Company (LLC) are known as members, who operate the business. These members invested money to own a stake in the business. There are different types of LLCs, are mostly based depending on the number of members and how they are managed. The owner also cannot escape breaking laws, repaying debts, and filing taxes. A multi-member LLC consists of multiple owners, and all owners need to agree to the rules governing the company.

In member-managed LLCs, the members manage the LLC according to the company rules. In this way, the members hire managers to operate the business in manager-managed LLCs where owners can entrust decisions that are important to the general manager.

LLC is different from PLLC. Professional limited liability companies (PLLCs) are for specific professions, such as accountants or doctors, where state regulations prohibit these professionals from forming regular LLCs.

Requirements of LLC

Member will first need to fill an Employer Identification Number (EIN) in the IRS to form an LLC. They will also need to select a unique business name and assign a registered agent. Depending on the state, members must then file a certificate of formation or articles of organization. This document generally contains the name of the LLC, the names of founding members or managers, the registered agent’s information, and a statement of the LLC’s purpose. The governing document to be used is typically filed with the secretary of state or a business agency for most states.

LLC Vs Other Business Structures

Sole Proprietorships

Sole proprietorships have complete control and pass-through taxation for the business owner but come with the unlimited personal liability of the business owner to pay all company debts.

Partnerships

There are multiple owners in a partnership who share the business’s assets, liabilities, and legal obligations with no limits on liabilities. An owner can have assets seized to pay debts, whereas an LLC isn’t a legal entity.

Corporations

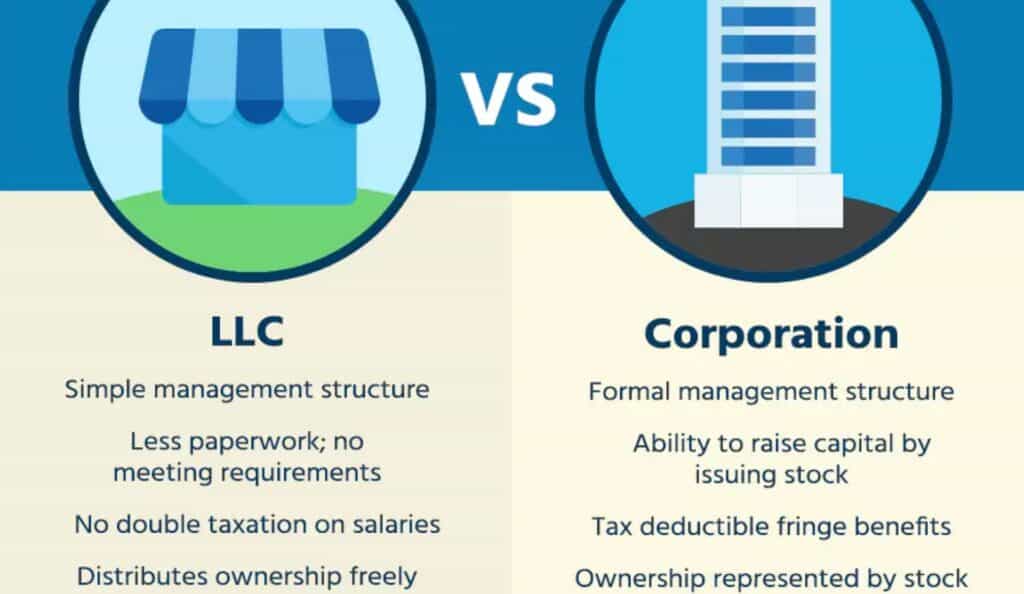

Where a corporation is a formal business that must adhere to stricter reporting rules, bureaucracy, and even shareholders, an LLC is more informal and does not require a board of directors. And while they are not corporations, LLCs can choose to be taxed and file taxes as such.

S Corporations

An S corporation is a type of business entity that uses pass-through taxation to transfer its income, losses, credits, and deductions to its owners. This enables shareholders to report their gains and losses on their individual income and tax returns at individual tax rates, thereby avoiding double taxation of corporate profits. S corporations have some pros.

Flexibility of LLCs

An LLC has less formal rules than a regular corporation, which makes it easier to manage. Rules for running an LLC are typically outlined in an operating agreement, which the members draft. In the absence of an agreement, state laws set forth basic rules.

Delaware law provides that managers and members of an LLC owe a duty of care to the LLC and its members. These duties may be changed in members’ agreements, but members still must act in good faith.

The operating agreement of a Delaware LLC may be written, oral, or implied by conduct. It specifies how much each member contributes, their ownership percentages, and how the company will be run. And it saves headaches down the road, covering aspects such as buy-out rights and how to value the business.

Like corporations, LLCs need to register in the states in which they do business. Small business owners may find the various rules confusing, as each state has its own definition of “doing business.” Sometimes an LLC formed in one state that does business in another would have to register again in that other state.

LLC and Legal Consideration

LLCs are governed by rules that shield members from personal liability for the debts and actions of the business. These set forth how the business operates, how income is distributed, and what reporting is required annually. LLCs are also required to enter into an agreement that describes how the business will operate, the roles of its members, and how profits will be distributed. The vast majority of states mandate annual reports.

Ordinary owners can invest in them, while some even accept new members who have deep pockets. Other terms like how members can exit, how to deal with offers to sell shares, and what happens if a member dies or isn’t able to continue, are also addressed in the agreement. It is necessary for management because it ensures that any changes to the company are made with all members in mutual agreement. Offshore LLCs are incorporated in foreign jurisdictions, so they are subject to the laws and taxes of those countries, which can bring additional fees or restrictions. It can be pricier and may require annual license renewals.

Conclusion

The limited liability company is a flexible business structure that provides liability protection, passes through taxation, and avoids many of the regulatory requirements of a traditional corporation. LLCs combine the benefits of sole proprietorships, partnerships, and corporations, so they can be useful for a variety of businesses.

But LLCs that are good for you may have disadvantages such as different state laws, fees, and the like, and funding difficulties. If done properly with formation, compliance, and an operating agreement that’s well drafted though, LLCs can be a good option regarding business growth and protection.